It’s a common practice here in the Philippines, that after the death of the ascendant or the bread winner, heirs usually sell their properties.

However, every time the property is sold, a problem arises when they will transfer the properties to the name of the buyer.

This commonly happens because most Filipinos are not aware of the concept of the estate tax. As a result, there are many properties for sale that are still under the name of the deceased person.

If the estate tax is not paid, the properties of the deceased cannot be transferred to another person.

This is a common problem of the Filipinos because the amount of the estate tax ranges from 5% to 20% based on the net estate of the deceased. Aside from this, it should be filed within six months. However, consideration is given based on the financial status of the heirs.

If it is your first time to hear this, you’d probably think that it’s a tax charge in a real estate property based on the first word “estate.” That’s about right but it’s more than just a real estate property.

What is Estate Tax?

The simplest way to define estate tax is, it’s a tax charge based on the net property of the deceased if it will be transferred to another person.

These properties include cars, real estate properties, business and other material and non-material properties with a total value of more than Php 200,000.00.

In other words, all properties below Php 200,000.00 can be inherited and are not subject to an estate tax.

How to Compute for Estate Tax?

To know how much is the is the net estate of your deceased relative you must compute for the gross estate. Gross Estate is the value of all the properties under his name at the time of death.

Next, is to deduct all the debt incurred by the deceased. Other than the debt, the following could also be deducted such as Taxes, Funeral Expenses, Medical Expenses, Share in the Conjugal Property etc.

Therefore, the formula is Gross Estate – Deductions = Net Estate.

Example

Assuming that the Gross Estate is Php 1 Million and the total deduction is Php 400,000.000. By using the formula,

1 Million – 400,000.00 = Php 600,000.00

The Net asset value is Php 600,000.00.

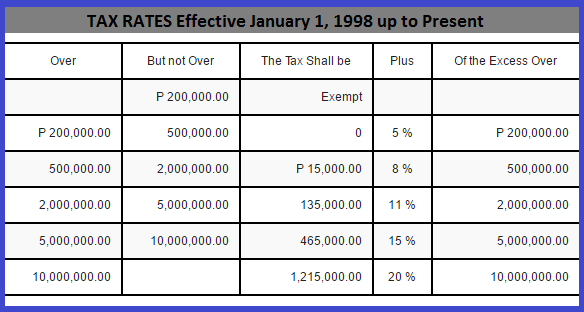

To determine the estate tax, we need to use the BIR Estate Tax Table.

Based on the table, the net estate Php 600,000.00, is within the range of Php 500,000.00 to Php 2,000,000.00.

Thus, the total estate tax to be paid will be Php 15,000.00 PLUS 8% of the net estate which is Php 48,000.00 because the amount exceeded Php 500,000.00.

Finally, the total amount to be paid for the estate tax will be Php 15,000.00 + Php 48,000.00 = Php 63,000.00.

In summary, this is the formula on how to compute for estate tax.

- ESTATE TAX = Net Estate + Plus (Percentage of the excess based on BIR Estate Tax Table)

- Net Estate = Gross Estate – Deductions

Based on the computation, the estate tax can be a burden on the part of the heirs of the deceased. However, there are legal ways on how to limit the amount of estate tax and this is called Estate Planning which can only be done when a person is still alive.

And just a reminder, in filing your estate tax, it’s best to consult first with a Public Attorney or Estate Tax Expert for proper guidance.

Personal exemption to Php20,000 should be part of deduction. Thanks

Question Saan po ba base and value ng lupa para mabayaran estate tax before selling ganoon po ba sa assesses value po ba regardless of how much I will sell it !! Thank you po

do I need to pay the estate tax bought from balikatan considering .it was a full payment since it was considered foreclose.

Hello po.. base sa given na 600k net estate.. di po ba ganito ang computation?

500000=15000

600000-500000=100000*.08=8000

=23000.00

thanks po..wait po ako reply.. salamat

What are the allowable deductions for the estate tax of my mother who died 4 years after the death of father. If not to much, kindly provide me a sample computation. Thanks.

My father died in 2000 my mother never filed an estate tax for their 2 conjugal properties recently my mother died and she has 3 properties under her own name (deeded by her parent) how do we compute/estimate estate tax, a single one using present rate under 2018 train law for 5 properties or separate computation (2 nos) one (1) each for my father (pre rain law rates) and mother (2018 rates)

It would be better po if you consult a Lawyer who handles Estate Taxes for accurate computations.

Hi! what if the decedent inherited a family home from his father who died just 8 months ago, is this considered as a property previously taxed if there are pertinent transfer taxes paid? What will happen to the deduction of family home, if this situation is considered as PPT? TIA

Legal/Tax Question: Estate/Inheritance Tax in the Philippines

Background:

Our deceased parents left our family house (both on title) in the Philippines, when they emigrated to the US in 1984 and became naturalized US citizens in 1989. Both resided in Hawaii until their death, father in June 2004 and mother in July 2009. Both died without a formal last will and testament.

Question:

1) How could the family house, owned by deceased parents who were naturalized US citizens, non-Philippine residents, without formal last will and testaments, be sold to settle all taxes and fees in the Philippines, and any leftover funds be distributed equally to eleven (11) children; ten (10) children are non-Philippine citizens and non-Philippine residents, and one (1) Filipino citizen, residing in the Philippines?

2) What are the tax implications for the eleven (11) children in the Philippines?

3) How could the individual shares of the ten (10) children be transferred out from the Philippines?